How Liquid Asset Based Lending (LABL) brings benefits to both banks and their customers

21 June 2019

Imagine you have a short-term cash need [university fees for your kids] but you do have some long-term bonds in your investments portfolio. Wouldn’t it be great if your bank allows you to temporarily block these assets and get a short term loan facility to bridge the gap?

Lending against liquid assets that customers hold within their bank, is an underexploited market opportunity. If delivered well with the right level of automation and self-service capability, it creates great value for banks and their customers. Below we give an overview of some of these benefits.

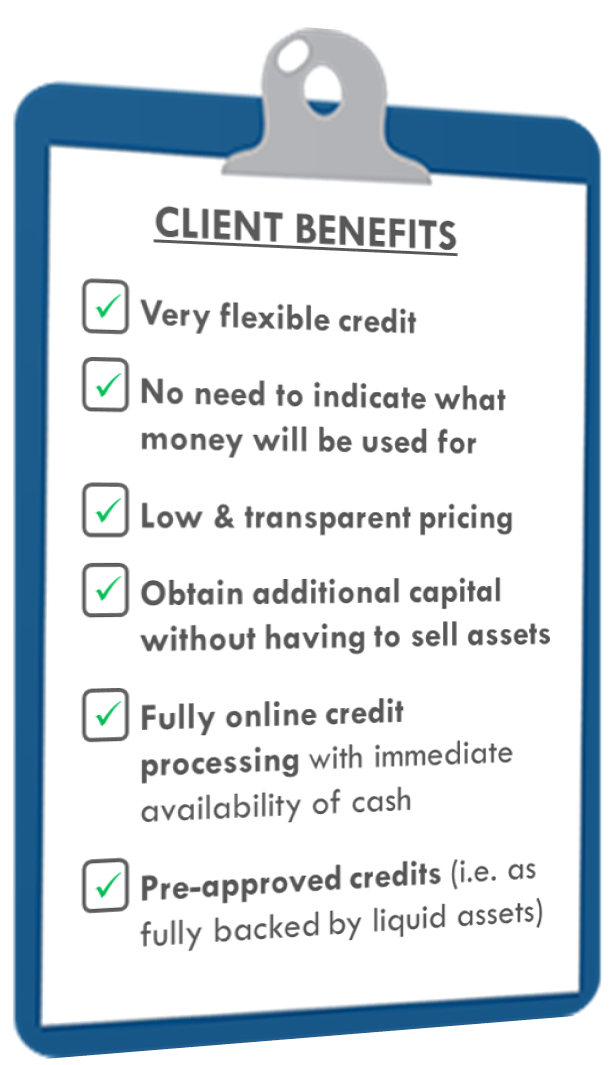

Bank customers get access to a flexible source of financing

Thanks to liquid asset based lending (LABL) customers can obtain a credit facility to bridge (short term) cash needs by blocking some of their (medium to long term) assets within the bank. By making this product available through self-service and online channels, customers get access to a very flexible (but still cheap) source of credit.

As credit scoring is entirely based on the underlying liquid assets – hence based on objective risk measurements – customers do not need to indicate what the money will be used for. Of course, for the setup of the initial contractual framework agreement or global LABL credit opening, standard credit bureau checks are to be performed, but afterwards the customer can flexibly open LABL loans as pre-approved loans, as they are fully covered by liquid assets. In addition, this objective scoring results in lower risk and hence lower and more transparent pricing of the credit: the interest rate only depends on the credit type (revolving vs. instalment) and duration, making it very easy for the client to predict costs.

Probably one of the most important benefits for end clients is the possibility to obtain additional capital without having to sell their existing assets, allowing these existing assets to continue generating income and capital increase without losing the mid-long term investment horizon.

As the focus for LABL is often on bridging short term cash needs, immediate pay-out of the credit amount is an important benefit for the end customer.

Banks improve their online service offering and generate new business

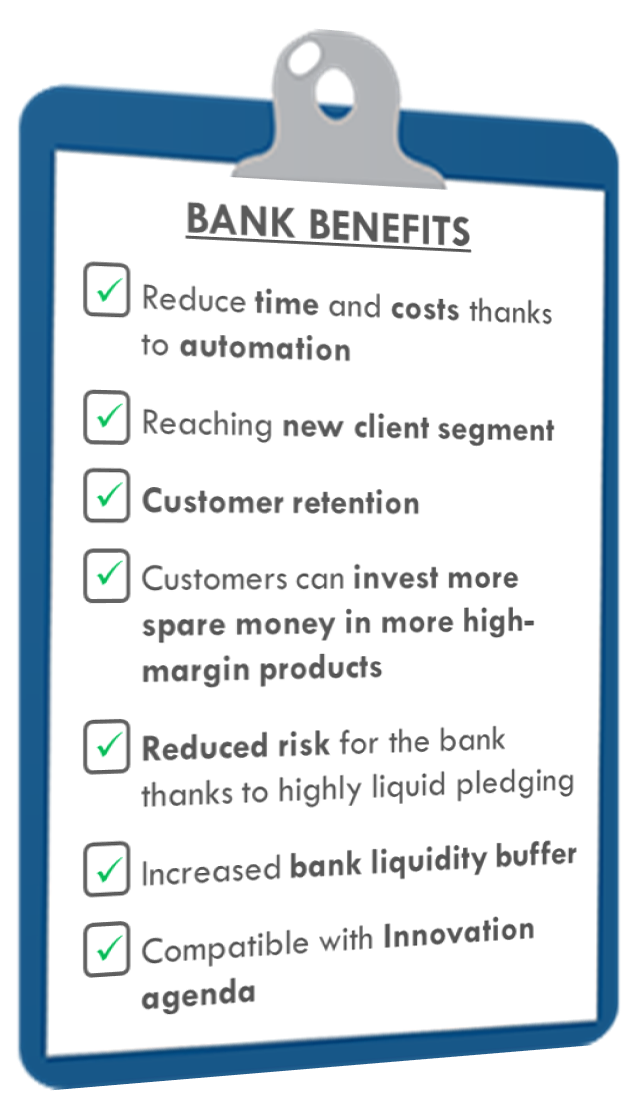

Banks are currently offering asset based loans only to private banking customers, due to the strong manual tailor-made nature of it. Automating this product can reduce time and costs for private banks, and help open up this product offering to a larger customer segment, thus considerably increasing the volume of credits sold (due to ease of credit and low prices). The target customer segment, holding assets (that don’t need to be liquidated in short-term), would normally (rarely) make use of credits, but instead sell off part of their investments or postpone their acquisition.

Offering LABL will also increase customer retention: while the credit is outstanding, the customer is not only linked to the bank for the credit, but also for the blocked collaterals (investments). Though this may change in the future when Open Banking APIs become available for credits and investments.

The bank customers will also invest more spare money in more high-margin products. Currently it is advised to keep up to 3 times your monthly spent in liquid assets. Via a low-priced, highly liquid and flexible source of credit, this could be reduced, so that customers can put more money in higher return assets with lower liquidity.

Thanks to highly liquid pledging, the risk for the bank is also significantly reduced. Credit scoring becomes independent of the individual client rating or due diligence, as mentioned above.

With LABL all credits are automatically covered by highly liquid assets, directly taking care of the stricter capital buffer requirements imposed by regulations (Basel II, III).

And last but not least, offering this new product is perfectly compatible with the innovation agenda of most banks, for example as part of their daily bank app or PFM/BFM solution. To reach larger retail audiences significant efforts are required for automating the different processes: for originating, servicing/monitoring and collecting of the LABL loans. Thanks to novel techniques and software approaches, this is now possible.