Liquid asset based lending – a clear retail banking market opportunity

Liquid asset based lending principle

18 Dec 2018

Lending against liquid marketable assets like securities and bonds, has been around for quite some time. We could say that the Lombards who conquered Italy in the 6th century, and settled in the northern region that became known as Lombardy, invented this first form of liquid asset based lending (LABL), often referred to as Lombard lending.

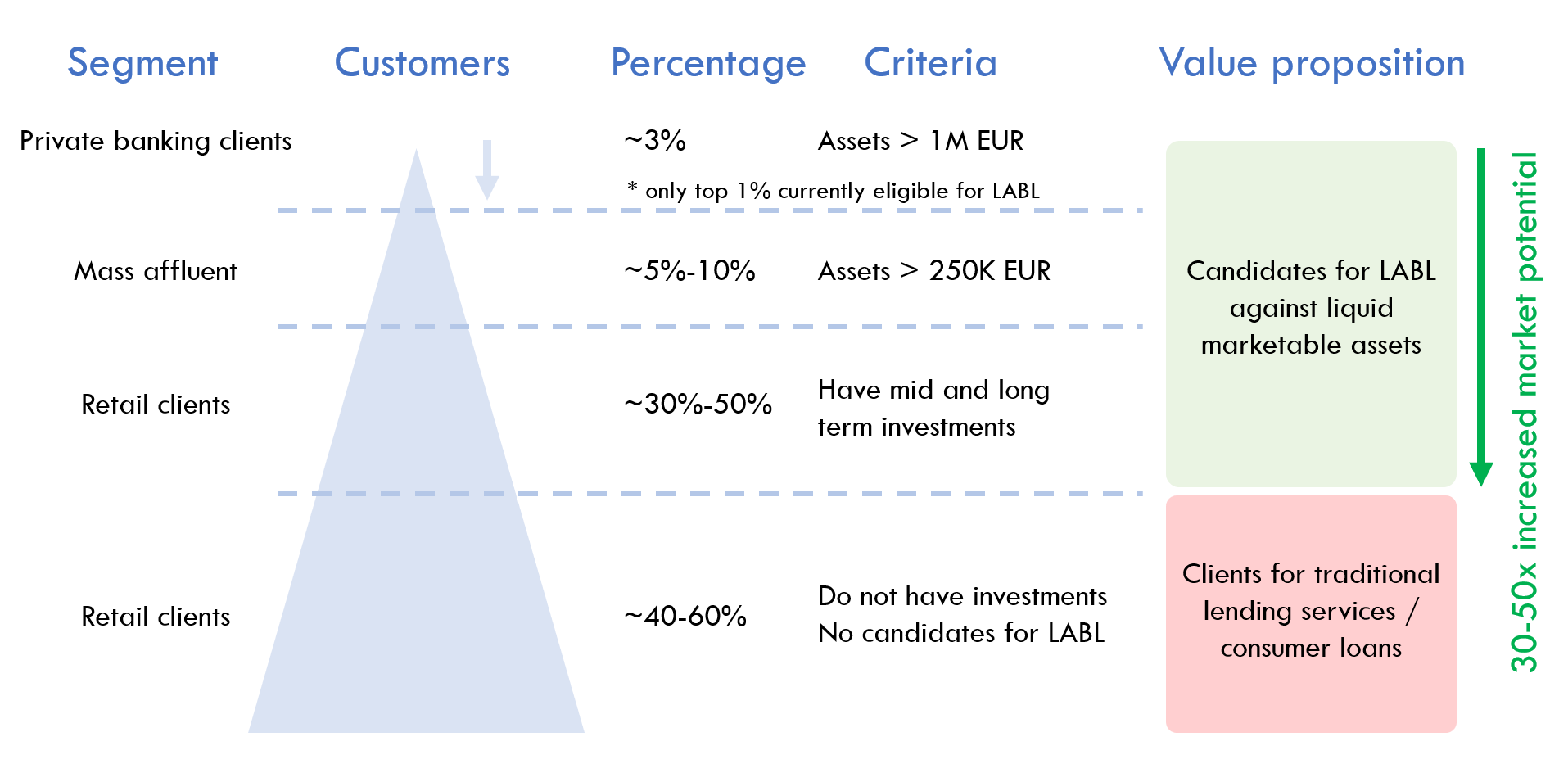

Nowadays, we find LABL or Lombard loans mostly in the private banking segment. High net worth individuals can borrow against some of their assets.

In the corporate space this type of lending facility is also frequently available, offering flexible credit lines and working capital for large corporates.

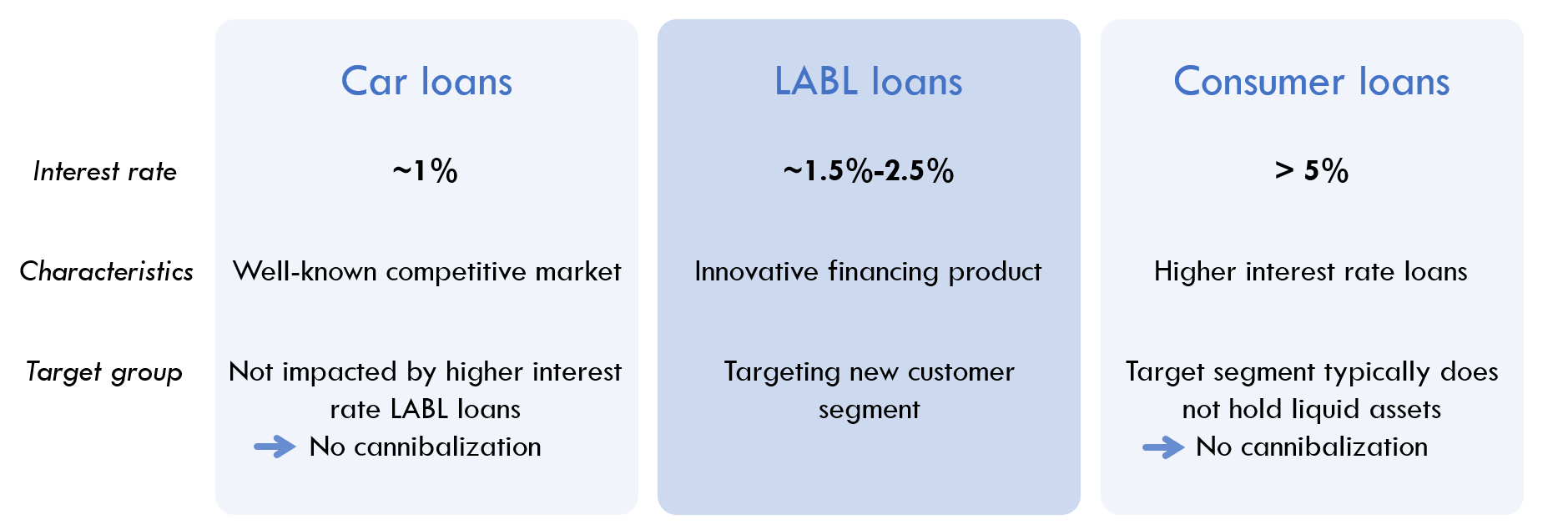

Finally a great opportunity is available in the retail and SME banking space.

A tier 1 bank in Belgium typically has about 3% of its customers in the private banking segment (more than 1,000,000 EUR in investable assets) and about 5-10% in the mass affluent segment (more than 250,000 EUR in investable assets). Currently only the top segment of the private banking customers is targeted for Lombard loans, resulting in less than 1% of the customers being targeted. If we consider that LABL loans can be interesting for any customer with assets, which don’t need to be liquidated in short-term (i.e. in term of less than 1 year), the target group does not only cover all private banking and mass affluent customers, but also a large part of the retail customers. For the same tier 1 bank, this can go to about 30-50% of the customer base, meaning that the target group is multiplied by a factor 30-50 compared to today’s situation. This shows a huge market potential.